7. Expectation, Averages, Variability

Summarizing Data on Random Variables

When we return midterm tests, someone almost always asks what the average was.

While we could list out all marks to give a picture of how students performed,

this would be tedious. It would also give more detail than could be

immediately digested. If we summarize the results by telling a class the

average mark, students immediately get a sense of how well the class

performed. For this reason, "summary statistics" are often more helpful than

giving full details of every outcome.

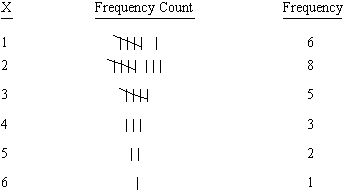

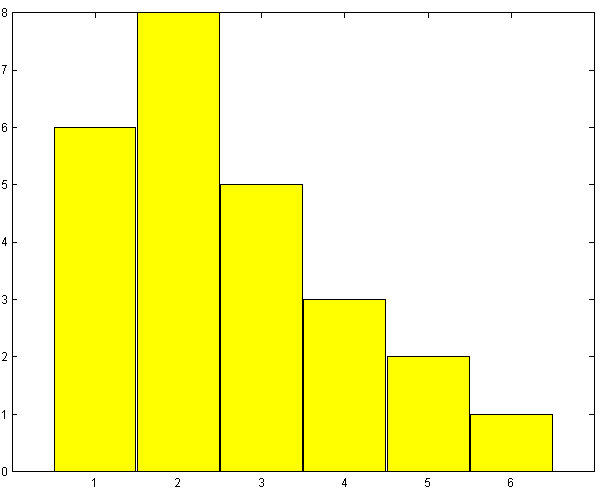

To illustrate some of the ideas involved, suppose we were to observe cars

crossing a toll bridge, and record the number,

,

of people in each car. Suppose in a small study data on 25 cars were

collected. We could list out all 25 numbers observed, but a more helpful way

of presenting the data would be in terms of the frequency

distribution below, which gives the number of times (the

``frequency'') each value of

,

of people in each car. Suppose in a small study data on 25 cars were

collected. We could list out all 25 numbers observed, but a more helpful way

of presenting the data would be in terms of the frequency

distribution below, which gives the number of times (the

``frequency'') each value of

occurred.

occurred.

We could also draw a frequency histogram of these

frequencies:

Frequency distributions or histograms are good summaries of data because they

show the variability in the observed outcomes very clearly. Sometimes,

however, we might prefer a single-number summary. The most common such summary

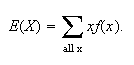

is the average, or arithmetic mean of the outcomes. The mean of

outcomes

outcomes

for a random variable

for a random variable

is

is

,

and is denoted by

,

and is denoted by

.

The arithmetic mean for the example above can be calculated as

.

The arithmetic mean for the example above can be calculated as

That is, there was an average of 2.6 persons per car. A set of observed

outcomes

That is, there was an average of 2.6 persons per car. A set of observed

outcomes

for a random variable

for a random variable

is termed a sample in probability and statistics. To reflect

the fact that this is the average for a particular sample, we refer to it as

the sample mean. Unless somebody deliberately "cooked" the

study, we would not expect to get precisely the same sample mean if we

repeated it another time. Note also that

is termed a sample in probability and statistics. To reflect

the fact that this is the average for a particular sample, we refer to it as

the sample mean. Unless somebody deliberately "cooked" the

study, we would not expect to get precisely the same sample mean if we

repeated it another time. Note also that

is not in general an integer, even though

is not in general an integer, even though

is.

is.

Two other common summary

statistics are the median and mode.

Definition

The median of a sample is a value such that half the results

are below it and half above it, when the results are arranged in numerical

order.

If these 25 results were written in order, the

outcome would be a 2. So the median is 2. By convention, we go half way

between the middle two values if there are an even number of observations.

outcome would be a 2. So the median is 2. By convention, we go half way

between the middle two values if there are an even number of observations.

Definition

The mode of the sample is the value which occurs most often.

In this case the mode is 2. There is no guarantee there will be only a single

mode.

Expectation of a Random Variable

The statistics in the preceding section summarize features of a sample of

observed

-values.

The same idea can be used to summarize the probability distribution of a

random variable

-values.

The same idea can be used to summarize the probability distribution of a

random variable

.

To illustrate, consider the previous example, where

.

To illustrate, consider the previous example, where

is the number of persons in a randomly selected car crossing a toll bridge.

is the number of persons in a randomly selected car crossing a toll bridge.

Note that we can re-arrange the expression used to calculate

for the sample,

as

for the sample,

as

Now suppose we know that the probability function of

Now suppose we know that the probability function of

is given by

is given by

|

1 |

2 |

3 |

4 |

5 |

6 |

|

.30 |

.25 |

.20 |

.15 |

.09 |

.01 |

Using the relative frequency ``definition'' of

probability, if we observed a very large number of cars, the fraction (or

relative frequency) of times

would be .30, for

would be .30, for

,

this proportion would be .25, etc. So, in theory,

(according to the probability model) we would expect the mean to be

,

this proportion would be .25, etc. So, in theory,

(according to the probability model) we would expect the mean to be

if we observed an infinite number of cars. This ``theoretical'' mean is

usually denoted by

if we observed an infinite number of cars. This ``theoretical'' mean is

usually denoted by

or

or

,

and requires us to know the distribution of

,

and requires us to know the distribution of

.

With this background we make the following mathematical

definition.

.

With this background we make the following mathematical

definition.

The expectation of

is also often denoted by the Greek letter

is also often denoted by the Greek letter

.

The expectation of

.

The expectation of

can be thought of physically as the average of the

can be thought of physically as the average of the

-values

that would occur in an infinite series of repetitions of the process where

-values

that would occur in an infinite series of repetitions of the process where

is defined. This value not only describes one aspect of a probability

distribution, but is also very important in certain types of applications. For

example, if you are playing a casino game in which

is defined. This value not only describes one aspect of a probability

distribution, but is also very important in certain types of applications. For

example, if you are playing a casino game in which

represents the amount you win in a single play, then

represents the amount you win in a single play, then

represents your average winnings (or losses!) per play.

represents your average winnings (or losses!) per play.

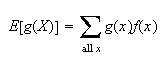

Sometimes we may not be interested in the average value of

itself, but in some function of

itself, but in some function of

.

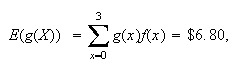

Consider the toll bridge example once again, and suppose there is a toll which

depends on the number of car occupants. For example, a toll of $1 per car plus

25 cents per occupant would produce an average toll for the 25 cars in the

study of Section 7.1 equal to

.

Consider the toll bridge example once again, and suppose there is a toll which

depends on the number of car occupants. For example, a toll of $1 per car plus

25 cents per occupant would produce an average toll for the 25 cars in the

study of Section 7.1 equal to

If

If

has the theoretical probability function

has the theoretical probability function

given above, then the average value of this $(.25X + 1) toll would be defined

in the same way, as,

given above, then the average value of this $(.25X + 1) toll would be defined

in the same way, as,

We call this the expectation of

and write

and write

.

.

As a further illustration, suppose a toll designed to encourage car pooling

charged

if there were

if there were

people in the car. This scheme would yield an average toll, in theory, of

people in the car. This scheme would yield an average toll, in theory, of

that

is, is the ``expectation'' of

is the ``expectation'' of

.

.

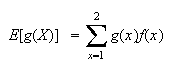

With this as background, we can now make a formal definition.

Notes:

-

You can interpret

![$E[g(X)]$](graphics/noteschap7__59.png) as the average value of

as the average value of

in an infinite series of repetitions of the process where

in an infinite series of repetitions of the process where

is defined.

is defined.

-

is also known as the ``expected value'' of

is also known as the ``expected value'' of

.

This name is somewhat misleading since the average value of

.

This name is somewhat misleading since the average value of

may be a value which

may be a value which

never takes - hence unexpected!

never takes - hence unexpected!

-

The case where

reduces to our earlier definition of

reduces to our earlier definition of

.

.

-

Confusion sometimes arises because we have two notations for the mean of a

probability distribution:

and

and

mean the same thing. There is nothing wrong with this.

mean the same thing. There is nothing wrong with this.

-

When calculating expectations, look at your answer to be sure it makes sense.

If

takes values from 1 to 10, you should know you've made an error if you get

takes values from 1 to 10, you should know you've made an error if you get

or

or

.

In physical terms,

.

In physical terms,

is the balance point for the histogram of

is the balance point for the histogram of

.

.

Let us note a couple of mathematical properties of expectation that can help

to simplify calculations.

Properties of Expectation:

If your linear algebra is good, it may help if you think of

as being a linear operator. Otherwise you'll have to remember these and

subsequent properties.

as being a linear operator. Otherwise you'll have to remember these and

subsequent properties.

-

For constants

and

and

,

,

Proof:

-

For constants

and

and

and functions

and functions

and

and

,

it is also easy to show

,

it is also easy to show

Don't let expectation intimidate you. Much of it is common sense. For example,

property 1 says

Don't let expectation intimidate you. Much of it is common sense. For example,

property 1 says

if we let

if we let

and

and

.

The expectation of a constant

.

The expectation of a constant

is of course equal to

is of course equal to

.

It also says

.

It also says

if we let

if we let

,

,

,

and

,

and

.

This is obvious also. Note, however, that for

.

This is obvious also. Note, however, that for

a nonlinear function, it is not true that

a nonlinear function, it is not true that

![$E[g(X)]=g(E(X))$](graphics/noteschap7__96.png) ;

this is a common mistake. (Check this for the example above when

;

this is a common mistake. (Check this for the example above when

.)

.)

Some Applications of Expectation

Because expectation is an average value, it is frequently used in problems

where costs or profits are connected with the outcomes of a random variable

.

It is also used a lot as a summary statistic for probability distributions;

for example, one often hears about the expected life (expectation of lifetime)

for a person or the expected return on an investment.

.

It is also used a lot as a summary statistic for probability distributions;

for example, one often hears about the expected life (expectation of lifetime)

for a person or the expected return on an investment.

The following are examples.

Example: Expected Winnings in a Lottery

A small lottery sells 1000 tickets numbered

;

the tickets cost $10 each. When all the tickets have been sold the draw takes

place: this consists of a simple ticket from 000 to 999 being chosen at

random. For ticket holders the prize structure is as follows:

;

the tickets cost $10 each. When all the tickets have been sold the draw takes

place: this consists of a simple ticket from 000 to 999 being chosen at

random. For ticket holders the prize structure is as follows:

-

Your ticket is drawn - win $5000.

-

Your ticket has the same first two number as the winning ticket, but the third

is different - win $100.

-

Your ticket has the same first number as the winning ticket, but the second

number is different - win $10.

-

All other cases - win nothing.

Let the random variable

represent the winnings from a given ticket. Find

represent the winnings from a given ticket. Find

.

.

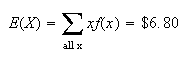

Solution: The possible values for

are 0, 10, 100, 5000 (dollars). First, we need to find the probability

function for

are 0, 10, 100, 5000 (dollars). First, we need to find the probability

function for

.

We find (make sure you can do this) that

.

We find (make sure you can do this) that

has values

has values

The expected winnings are thus the expectation of

,

or

,

or

Thus, the gross expected winnings per ticket are $6.80. However, since a

ticket costs $10 your expected net winnings are negative, -$3.20 (i.e. an

expected loss of $3.20).

Thus, the gross expected winnings per ticket are $6.80. However, since a

ticket costs $10 your expected net winnings are negative, -$3.20 (i.e. an

expected loss of $3.20).

Remark: For any lottery or game of chance the expected net

winnings per play is a key value. A fair game is one for which this value is

0. Needless to say, casino games and lotteries are never fair: the net

winnings for a player are

negative.

Remark: The random variable associated with a given

problem may be defined in different ways but the expected winnings will remain

the same. For example, instead of defining

as the amount won we could have defined

as the amount won we could have defined

as follows:

as follows:

|

|

all 3 digits of number match winning ticket |

|

|

1st 2 digits (only) match |

|

|

1st digit (but not the 2nd) match |

|

|

1st digit does not match |

Now, we would define the function

as the winnings when the outcome

as the winnings when the outcome

occurs. Thus,

occurs. Thus,

The expected winnings are then

the same as before.

the same as before.

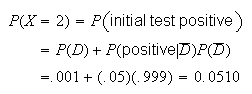

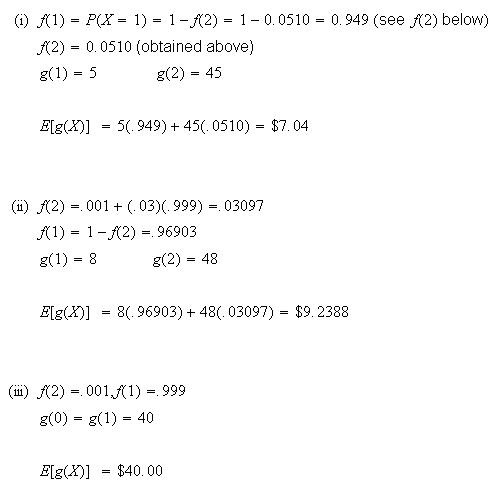

Example: Diagnostic Medical Tests

Often there are cheaper, less accurate tests for diagnosing the presence of

some conditions in a person, along with more expensive, accurate tests.

Suppose we have two cheap tests and one expensive test, with the following

characteristics. All three tests are positive if a person has the condition

(there are no "false negatives"), but the cheap tests give "false positives".

Let a person be chosen at random, and let

= {person has the condition}. The three tests are

= {person has the condition}. The three tests are

| Test 1: |

|

(positive test

(positive test

= .05; test costs $5.00

= .05; test costs $5.00 |

| Test 2: |

|

(positive test

(positive test

= .03; test costs $8.00

= .03; test costs $8.00 |

| Test 3: |

|

(positive test

(positive test

= 0; test costs $40.00

= 0; test costs $40.00 |

We want to check a large number of people for the condition, and have to

choose among three testing strategies:

-

Use Test 1, followed by Test 3 if Test 1 is positive.

-

Use Test 2, followed by Test 3 if Test 2 is positive.

-

Use Test 3.

Determine the expected cost per person under each of strategies (i), (ii) and

(iii). We will then choose the strategy with the lowest expected cost. It is

known that about .001 of the population have the condition (i.e.

).

).

Solution: Define the random variable

as follows (for a random person who is tested):

as follows (for a random person who is tested):

|

|

if the initial test is negative |

|

|

if the initial test is positive |

Also let

be the total cost of testing the person. The expected cost per person is then

be the total cost of testing the person. The expected cost per person is then

The probability function

for

for

and function

and function

differ for strategies (i), (ii) and (iii). Consider for example strategy (i).

Then

differ for strategies (i), (ii) and (iii). Consider for example strategy (i).

Then

The rest if the probabilities, associated values of

The rest if the probabilities, associated values of

and

and

![$E[g(X)]$](graphics/noteschap7__140.png) are obtained below.

are obtained below.

Thus, its cheapest to use strategy

(i).

Problem:

-

A lottery has tickets numbered 000 to 999 which are sold for $1 each. One

ticket is selected at random and a prize of $200 is given to any person whose

ticket number is a permutation of the selected ticket number. All 1000 tickets

are sold. What is the expected profit or loss to the organization running the

lottery?

Means and Variances of Distributions

Its useful to know the means,

of probability models derived in Chapter

6.

of probability models derived in Chapter

6.

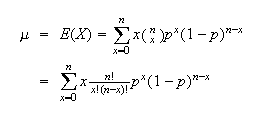

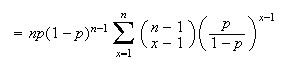

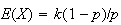

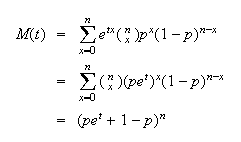

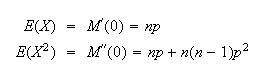

Example: (Mean of binomial distribution)

Let

.

Find

.

Find

.

.

Solution:

When

the value of the expression is 0. We can therefore begin our sum at

the value of the expression is 0. We can therefore begin our sum at

.

Provided

.

Provided

,

we can expand

,

we can expand

as

as

(so it is important to eliminate the term when

(so it is important to eliminate the term when

).

).

Let

Let

in the sum, to get

in the sum, to get

Exercise: Does this result make sense? If you try something

100 times and there is a 20% chance of success each time, how many successes

do you expect to get, on

average?

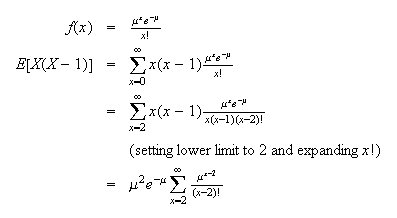

Example: (Mean of the Poisson

distribution)

Let

have a Poisson distribution where

have a Poisson distribution where

is the average rate of occurrence and the time interval is of length

is the average rate of occurrence and the time interval is of length

.

Find

.

Find

.

.

Solution:

The probability function of

is

is

.

Then

.

Then

.

.

As in the binomial example, we can eliminate the term when

and expand

and expand

as

as

for

for

.

.

Let

Let

in the sum.

in the sum.

Note that we used the symbol

Note that we used the symbol

earlier in connection with the Poisson model; this was because we knew (but

couldn't show until now) that

earlier in connection with the Poisson model; this was because we knew (but

couldn't show until now) that

.

.

Exercise: These techniques can also be used to work out the

mean for the hypergeometric or negative binomial distributions. Looking back

at how we proved that

shows the same method of summation used to find

shows the same method of summation used to find

.

However, in Chapter 8 we will give a simpler method of finding the means of

these distributions, which are

.

However, in Chapter 8 we will give a simpler method of finding the means of

these distributions, which are

(hypergeometric) and

(hypergeometric) and

(negative binomial).

(negative binomial).

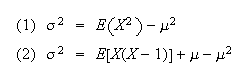

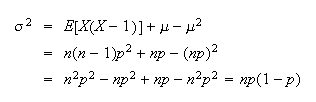

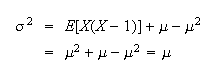

Variability:

While an average is a useful summary of a set of observations, or of a

probability distribution, it omits another important piece of information,

namely the amount of variability. For example, it would be possible for car

doors to be the right width, on average, and still have no doors fit properly.

In the case of fitting car doors, we would also want the door widths to all be

close to this correct average. We give a way of measuring the amount of

variability next. You might think we could use the average difference between

and

and

to indicate the amount of variation. In terms of expectation, this would be

to indicate the amount of variation. In terms of expectation, this would be

.

However,

.

However,

(since

(since

is a constant) = 0. We soon realize that to measure variability we need a

function that is the same sign for

is a constant) = 0. We soon realize that to measure variability we need a

function that is the same sign for

and for

and for

.

We now define

.

We now define

In words, the variance is the

average square of the distance from the mean. This turns out to be a very

useful measure of the variability of

.

.

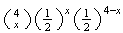

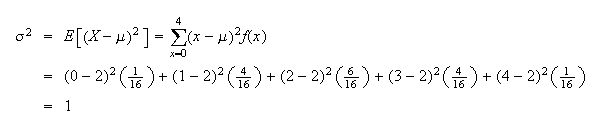

Example: Let

be the number of heads when a fair coin is tossed 4 times. Then

be the number of heads when a fair coin is tossed 4 times. Then

so

so

.

Without doing any calculations we know

.

Without doing any calculations we know

because

because

is always between 0 and 4. Hence it can never be further away from

is always between 0 and 4. Hence it can never be further away from

than 2. This makes the average square of the distance from

than 2. This makes the average square of the distance from

at most 4. The values of

at most 4. The values of

are

are

|

0 |

1 |

2 |

3 |

4 |

since

|

= |

|

|

1/16 |

4/16 |

6/16 |

4/16 |

1/16 |

|

= |

|

The value of

(i.e.

(i.e.

)

is easily found here:

)

is easily found here:

If we keep track of units of

measurement the variance will be in peculiar units; e.g. if

is the number of heads in 4 tosses of a coin,

is the number of heads in 4 tosses of a coin,

is in units of

heads

is in units of

heads !

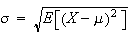

We can regain the original units by taking (positive)

!

We can regain the original units by taking (positive)

.

This is called the standard deviation of

.

This is called the standard deviation of

,

and is denoted by

,

and is denoted by

,

or as

,

or as

.

.

Definition

The standard deviation of a random variable

is

is

Both variance and standard

deviation are commonly used to measure variability.

The basic definition of

variance is often awkward to use for mathematical calculation of

,

whereas the following two results are often useful:

,

whereas the following two results are often useful:

Proof:

-

Using properties of expectation,

(2)

Formula (2) is most often used when there is an

term in the denominator of

term in the denominator of

.

Otherwise, formula (1) is generally easier to

use.

.

Otherwise, formula (1) is generally easier to

use.

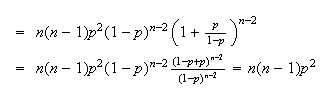

Example: (Variance of binomial distribution)

Let

.

Find Var

.

Find Var

Solution:

,

so we'll use formula (2).

,

so we'll use formula (2).

If

or

or

the value of the term is 0, so we can begin summing at

the value of the term is 0, so we can begin summing at

.

For

.

For

or

or

,

we can expand the

,

we can expand the

as

as

Now re-group to fit the binomial theorem, since that was the summation

technique used to show

Now re-group to fit the binomial theorem, since that was the summation

technique used to show

and to derive

and to derive

.

.

Let

Let

in the sum, giving

in the sum, giving

Then

Then

Remember that the variance of a binomial distribution is

Remember that the variance of a binomial distribution is

,

since we'll be using it later in the

course.

,

since we'll be using it later in the

course.

Example: (Variance of Poisson distribution) Find the

variance of the Poisson distribution.

Solution:

Let

Let

in the sum, giving

in the sum, giving

(that is, for the Poisson, the variance equals the

mean.)

(that is, for the Poisson, the variance equals the

mean.)

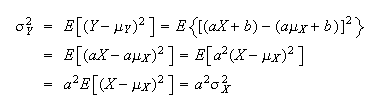

Properties of Mean and Variance

If

and

and

are constants and

are constants and

,

then

,

then

(where

and

and

are the mean and variance of

are the mean and variance of

and

and

and

and

are the mean and variance of

are the mean and variance of

).

).

Proof:

We already showed that

.

.

i.e.

,

and then

,

and then

This result is to be expected. Adding a constant,

,

to all values of

,

to all values of

has no effect on the amount of variability. So it makes sense that Var

has no effect on the amount of variability. So it makes sense that Var

doesn't depend on the value of

doesn't depend on the value of

.

.

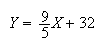

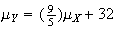

A simple way to relate to this result is to consider a random variable

which represents a temperature in degrees Celsius (even though this is a

continuous random variable which we don't study until Chapter 9). Now let

which represents a temperature in degrees Celsius (even though this is a

continuous random variable which we don't study until Chapter 9). Now let

be the corresponding temperature in degrees Fahrenheit. We know that

be the corresponding temperature in degrees Fahrenheit. We know that

and it is clear if we think about it that

and it is clear if we think about it that

and that

and that

.

.

Problems:

-

An airline knows that there is a 97% chance a passenger for a certain flight

will show up, and assumes passengers arrive independently of each other.

Tickets cost $100, but if a passenger shows up and can't be carried on the

flight the airline has to refund the $100 and pay a penalty of $400 to each

such passenger. How many tickets should they sell for a plane with 120 seats

to maximize their expected ticket revenues after paying any penalty charges?

Assume ticket holders who don't show up get a full refund for their unused

ticket.

-

A typist typing at a constant speed of 60 words per minute makes a mistake in

any particular word with probability .04, independently from word to word.

Each incorrect word must be corrected; a task which takes 15 seconds per word.

-

Find the mean and variance of the time (in seconds) taken to finish a 450 word

passage.

-

Would it be less time consuming, on average, to type at 45 words per minute if

this reduces the probability of an error to .02?

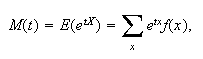

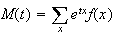

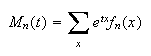

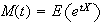

Moment Generating Functions

We have now seen two functions which characterize a distribution, the

probability function and the cumulative distribution function. There is a

third type of function, the moment generating

function, which uniquely determines a distribution. The moment

generating function is closely related to other transforms used in

mathematics, the Laplace and Fourier transforms.

The moments of a random variable

are the expectations of the functions

are the expectations of the functions

for

for

.

The expectation

.

The expectation

is called

is called

moment of

moment of

.

The mean

.

The mean

is therefore the first moment,

is therefore the first moment,

the second and so on. It is often easy to find the moments of a probability

distribution mathematically by using the moment generating function. This

often gives easier derivations of means and variances than the direct

summation methods in the preceding section. The following theorem gives a

useful property of m.g.f.'s.

the second and so on. It is often easy to find the moments of a probability

distribution mathematically by using the moment generating function. This

often gives easier derivations of means and variances than the direct

summation methods in the preceding section. The following theorem gives a

useful property of m.g.f.'s.

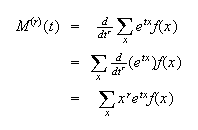

Proof:

and if the sum converges, then

and if the sum converges, then

,

as stated.

,

as stated.

This sometimes gives a simple way to find the moments for a distribution.

Example 1.

![MATH]()

and

so

From this we can also find

From this we can also find

Exercise. Poisson distribution

Show that the Poisson distribution with probability function

has m.g.f.

has m.g.f.

.

Then show that

.

Then show that

and

and

.

.

The m.g.f. also uniquely

identifies a distribution in the sense that two different distributions cannot

have the same m.g.f. This result is often used to find the distribution of a

random variable.

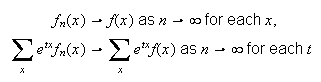

The other feature of the moment generating function that is often used is that

it can be used to identify a given distribution. If two random variables have

the same moment generating function, they have the same distribution (so the

same probability function, cumulative distribution function, moments, etc.)

But in fact moment generating functions can also be used to determine that a

sequence of distributions gets closer and closer to some limiting

distribution. To show this, suppose that a sequence of probability functions

have corresponding moment generating functions

have corresponding moment generating functions

Suppose moreover that the probability functions

Suppose moreover that the probability functions

converge to another probability function

converge to another probability function

pointwise in

pointwise in

as

as

.

This is what we mean by convergence of discrete distributions. Then since

.

This is what we mean by convergence of discrete distributions. Then since

which says that

which says that

converges to

converges to

the moment generating function of the limiting distribution. It shouldn't be

too surprising that a very useful converse to this result also holds:

the moment generating function of the limiting distribution. It shouldn't be

too surprising that a very useful converse to this result also holds:

Suppose

has moment generating function

has moment generating function

and

and

for each

for each

such that

such that

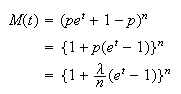

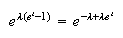

For example we saw in Chapter 6 that a

Binomial

For example we saw in Chapter 6 that a

Binomial distribution with very large

distribution with very large

and very small

and very small

is close to a Poisson distribution with parameter

is close to a Poisson distribution with parameter

Consider the moment generating function of such a binomial random

variable

Consider the moment generating function of such a binomial random

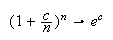

variable Now consider the limit of this expression as

Now consider the limit of this expression as

Since in general

Since in general

the limit of (binmgf) as

the limit of (binmgf) as

is

is

and this is the moment generating function of a Poisson distribution with

parameter

and this is the moment generating function of a Poisson distribution with

parameter

This shows a little more formally than we did earlier that the

binomial

This shows a little more formally than we did earlier that the

binomial distribution with

distribution with

approaches the

Poisson(

approaches the

Poisson( )

distribution as

)

distribution as

Problems on Chapter 7

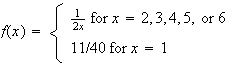

-

Let

have probability function

have probability function

Find the mean and variance for

Find the mean and variance for

.

.

-

A game is played where a fair coin is tossed until the first tail occurs. The

probability

tosses will be needed is

tosses will be needed is

.

You win

.

You win

if

if

tosses are needed for

tosses are needed for

but lose $256 if

but lose $256 if

.

Determine your expected winnings.

.

Determine your expected winnings.

-

Diagnostic tests. Consider diagnostic tests like those discussed above in the

example of Section 7.3 and in Problem 15 for Chapter 4. Assume that for a

randomly selected person,

,

,

,

,

,

so that the inexpensive test only gives false positive, and not false

negative, results.

,

so that the inexpensive test only gives false positive, and not false

negative, results.

Suppose that this inexpensive test costs $10. If a

person tests positive then they are also given a more expensive test, costing

$100, which correctly identifies all persons with the disease. What is the

expected cost per person if a population is tested for the disease using the

inexpensive test followed, if necessary, by the expensive test?

-

Diagnostic tests II. Two percent of the population has a certain condition for

which there are two diagnostic tests. Test A, which costs $1 per person, gives

positive results for 80% of persons with the condition and for 5% of persons

without the condition. Test B, which costs $100 per person, gives positive

results for all persons with the condition and negative results for all

persons without it.

-

-

Suppose that test B is given to 150 persons, at a cost of $15,000. How many

cases of the condition would one expect to detect?

-

Suppose that 2000 persons are given test A, and then only those who test

positive are given test B. Show that the expected cost is $15,000 but that the

expected number of cases detected is much larger than in part (a).

-

The probability that a roulette wheel stops on a red number is 18/37. For each

bet on ``red'' you win the amount bet if the wheel stops on a red number, and

lose your money if it does not.

-

-

If you bet $1 on each of 10 consecutive plays, what is your expected winnings?

What is your expected winnings if you bet $10 on a single play?

-

For each of the two cases in part (a), calculate the probability that you made

a profit (that is, your ``winnings'' are positive, not negative).

-

Slot machines. Consider the slot machine discussed above in Problem 16 for

Chapter 4. Suppose that the number of each type of symbol on wheels 1, 2 and 3

is as given below:

| |

|

Wheel |

| |

|

|

|

|

| Symbols |

|

1 |

2 |

3 |

|

Flower |

|

2 |

6 |

2 |

|

Dog |

|

4 |

3 |

3 |

|

House |

|

4 |

1 |

5 |

If all three wheels stop on a flower, you win $20 for a $1 bet. If all three

wheels stop on a dog, you win $10, and if all three stop on a house, you win

$5. Otherwise you win nothing.

Find your expected winnings per dollar spent.

-

Suppose that

people take a blood test for a disease, where each person has probability

people take a blood test for a disease, where each person has probability

of having the disease, independent of other persons. To save time and money,

blood samples from

of having the disease, independent of other persons. To save time and money,

blood samples from

people are pooled and analyzed together. If none of the

people are pooled and analyzed together. If none of the

persons has the disease then the test will be negative, but otherwise it will

be positive. If the pooled test is positive then each of the

persons has the disease then the test will be negative, but otherwise it will

be positive. If the pooled test is positive then each of the

persons is tested separately (so

persons is tested separately (so

tests are done in that case).

tests are done in that case).

-

-

A manufacturer of car radios ships them to retailers in cartons of

radios. The profit per radio is $59.50, less shipping cost of $25 per carton,

so the profit is $

radios. The profit per radio is $59.50, less shipping cost of $25 per carton,

so the profit is $

per carton. To promote sales by assuring high quality, the manufacturer

promises to pay the retailer

per carton. To promote sales by assuring high quality, the manufacturer

promises to pay the retailer

if

if

radios in the carton are defective. (The retailer is then responsible for

repairing any defective radios.) Suppose radios are produced independently and

that 5% of radios are defective. How many radios should be packed per carton

to maximize expected net profit per carton?

radios in the carton are defective. (The retailer is then responsible for

repairing any defective radios.) Suppose radios are produced independently and

that 5% of radios are defective. How many radios should be packed per carton

to maximize expected net profit per carton?

-

Let

have a geometric distribution with probability

function

have a geometric distribution with probability

function

-

-

Calculate the m.g.f.

,

where

,

where

is a parameter.

is a parameter.

-

Find the mean and variance of

.

.

-

Use your result in (b) to show that if

is the probability of ``success''

(

is the probability of ``success''

( )

in a sequence of Bernoulli trials, then the expected number of trials until

the first

)

in a sequence of Bernoulli trials, then the expected number of trials until

the first

occurs is

occurs is

.

Explain why this is ``obvious''.

.

Explain why this is ``obvious''.

-

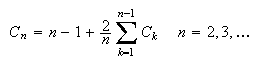

Analysis of Algorithms: Quicksort. Suppose we have a set

of distinct numbers and we wish to sort them from smallest to largest. The

quicksort algorithm works as follows: When

of distinct numbers and we wish to sort them from smallest to largest. The

quicksort algorithm works as follows: When

it just compares the numbers and puts the smallest one first. For

it just compares the numbers and puts the smallest one first. For

it starts by choosing a random "pivot" number from the

it starts by choosing a random "pivot" number from the

numbers. It then compares each of the other

numbers. It then compares each of the other

numbers with the pivot and divides them into groups

numbers with the pivot and divides them into groups

(numbers smaller than the pivot) and

(numbers smaller than the pivot) and

( numbers bigger than the pivot). It then does the same thing with

( numbers bigger than the pivot). It then does the same thing with

and

and

as it did with

as it did with

,

and repeats this recursively until the numbers are all sorted. (Try this out

with, say

,

and repeats this recursively until the numbers are all sorted. (Try this out

with, say

numbers to see how it works.) In computer science it is common to analyze such

algorithms by finding the expected number of comparisons (or other operations)

needed to sort a list. Thus, let

numbers to see how it works.) In computer science it is common to analyze such

algorithms by finding the expected number of comparisons (or other operations)

needed to sort a list. Thus, let

-

Show that if

is the number of comparisons needed,

is the number of comparisons needed,

-

Show that

and thus that

and thus that

satisfies the recursion (note

satisfies the recursion (note

)

)

-

Show that

-

(Harder) Use the result of part (c) to show that for large

,

,

(Note:

(Note:

means

means

as

as

)

This proves a result from computer science which says that for Quicksort,

)

This proves a result from computer science which says that for Quicksort,

.

.

-

Find the distributions that corresponds to the following moment-generating

functions:

(a)

(b)

-

Find the moment generating function of the discrete uniform distribution

on

on

;

;

What do you get in the special case

What do you get in the special case

and in the case

and in the case

Use the moment generating function in these two cases to confirm the expected

value and the variance of

Use the moment generating function in these two cases to confirm the expected

value and the variance of

-

Let

be a random variable taking values in the set

be a random variable taking values in the set

with moments

with moments

,

,

-

Find the moment generating function of

-

Find the first six moments of

-

Find

-

Show that any probability distribution on

is completely determined by its first two moments.

is completely determined by its first two moments.