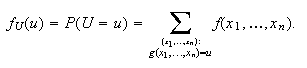

8. Discrete Multivariate Distributions

Basic Terminology and Techniques

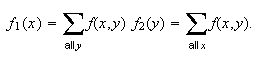

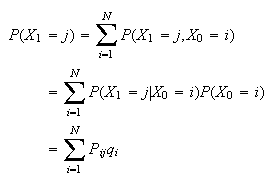

Many problems involve more than a single random variable. When there are

multiple random variables associated with an experiment or process we usually

denote them as

or as

or as

.

For example, your final mark in a course might involve

.

For example, your final mark in a course might involve

-- your assignment mark,

-- your assignment mark,

-- your midterm test mark, and

-- your midterm test mark, and

-- your exam mark. We need to extend the ideas introduced for single variables

to deal with multivariate problems. In this course we only consider discrete

multivariate problems, though continuous multivariate variables are also

common in daily life (e.g. consider a person's height

-- your exam mark. We need to extend the ideas introduced for single variables

to deal with multivariate problems. In this course we only consider discrete

multivariate problems, though continuous multivariate variables are also

common in daily life (e.g. consider a person's height

and weight

and weight

).

).

To introduce the ideas in a simple setting, we'll first consider an example in

which there are only a few possible values of the variables. Later we'll apply

these concepts to more complex examples. The ideas themselves are simple even

though some applications can involve fairly messy algebra.

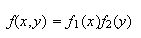

Joint Probability Functions:

First, suppose there are two r.v.'s

and

and

,

and define the function

,

and define the function

We call

the joint probability function of

the joint probability function of

.

In general,

.

In general,

if there are

if there are

r.v.'s

r.v.'s

.

.

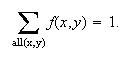

The properties of a joint probability function are similar to those for a

single variable; for two r.v.'s we have

for all

for all

and

and

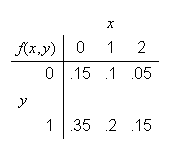

Example: Consider the following numerical example, where we

show

in a table.

in a table.

|

|

|

|

0 |

1 |

2 |

|

1 |

.1 |

.2 |

.3 |

|

|

|

|

|

|

2 |

.2 |

.1 |

.1 |

for example

and

and

We can check that

is a proper joint probability function since

is a proper joint probability function since

for all 6 combinations of

for all 6 combinations of

and the sum of these 6 probabilities is 1. When there are only a few values

for

and the sum of these 6 probabilities is 1. When there are only a few values

for

and

and

it is often easier to tabulate

it is often easier to tabulate

than to find a formula for it. We'll use this example below to illustrate

other definitions for multivariate distributions, but first we give a short

example where we need to find

than to find a formula for it. We'll use this example below to illustrate

other definitions for multivariate distributions, but first we give a short

example where we need to find

.

.

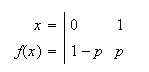

Example: Suppose a fair coin is tossed 3 times. Define the

r.v.'s

= number of Heads and

= number of Heads and

if

if

occurs on the first toss. Find the joint probability function for

occurs on the first toss. Find the joint probability function for

.

.

Solution: First we should note the range for

,

which is the set of possible values

,

which is the set of possible values

which can occur. Clearly

which can occur. Clearly

can be 0, 1, 2, or 3 and

can be 0, 1, 2, or 3 and

can be 0 or 1, but we'll see that not all 8 combinations

can be 0 or 1, but we'll see that not all 8 combinations

are possible.

are possible.

We can find

by just writing down the sample space

by just writing down the sample space

that we have used before for this process. Then simple counting gives

that we have used before for this process. Then simple counting gives

as shown in the following table:

as shown in the following table:

For example,

iff the outcome is

iff the outcome is

iff the outcome is either

iff the outcome is either

or

or

.

.

Note that the range or joint p.f. for

is a little awkward to write down here in formulas, so we just use the

table.

is a little awkward to write down here in formulas, so we just use the

table.

Marginal Distributions:

We may be given a joint probability function involving more variables than

we're interested in using. How can we eliminate any which are not of interest?

Look at the first example above. If we're only interested in

,

and don't care what value

,

and don't care what value

takes, we can see that

takes, we can see that

so

so

Similarly

Similarly

and

and

The distribution of

obtained in this way from the joint distribution is called the marginal

probability function of

obtained in this way from the joint distribution is called the marginal

probability function of

:

:

|

0 |

1 |

2 |

|

.3 |

.3 |

.4 |

In the same way, if we were only interested in

,

we obtain

,

we obtain

since

since

can be 0, 1, or 2 when

can be 0, 1, or 2 when

.

The marginal probability function of

.

The marginal probability function of

would be:

would be:

|

1 |

2 |

|

.6 |

.4 |

Our notation for marginal probability functions is still inadequate. What is

?

As soon as we substitute a number for

?

As soon as we substitute a number for

or

or

,

we don't know which variable we're referring to. For this reason, we generally

put a subscript on the

,

we don't know which variable we're referring to. For this reason, we generally

put a subscript on the

to indicate whether it is the marginal probability function for the first or

second variable. So

to indicate whether it is the marginal probability function for the first or

second variable. So

would be

would be

,

while

,

while

would be

would be

.

.

In general, to find

we add over all values of

we add over all values of

where

where

,

and to find

,

and to find

we add over all values of

we add over all values of

with

with

.

Then

.

Then

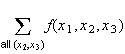

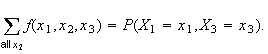

This reasoning can be extended beyond two variables. For example, with 3

variables

,

,

-

would be

would be

and

and

-

would be

would be

Independent Random Variables:

For events

and

and

,

we have defined

,

we have defined

and

and

to be independent

iff

to be independent

iff

.

This definition can be extended to random variables

.

This definition can be extended to random variables

Definition

In general,

are independent random variables

iff

are independent random variables

iff

In our first example

and

and

are not independent since

are not independent since

for any of the 6 combinations of

for any of the 6 combinations of

values; e.g.,

values; e.g.,

but

but

.

Be careful applying this definition. You can only conclude that

.

Be careful applying this definition. You can only conclude that

and

and

are independent after checking

all

are independent after checking

all  combinations. Even a single case where

combinations. Even a single case where

makes

makes

and

and

dependent.

dependent.

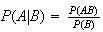

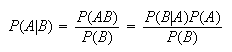

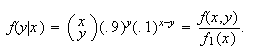

Conditional Probability Functions:

Again we can extend a definition from events to random variables. For events

and

and

,

recall that

,

recall that

.

Since

.

Since

,

we make the following definition.

,

we make the following definition.

In our first example let us

find

.

.

This gives:

This gives:

As you would expect, marginal and conditional probability functions are

probability functions in that they are always

and their sum is 1.

and their sum is 1.

Functions of Variables:

In an example earlier, your final mark in a course might be a function of the

3 variables

- assignment, midterm, and exam

marks Note_1 . Indeed, we often

encounter problems where we need to find the probability distribution of a

function of two or more r.v.'s. The most general method for finding the

probability function for some function of random variables

- assignment, midterm, and exam

marks Note_1 . Indeed, we often

encounter problems where we need to find the probability distribution of a

function of two or more r.v.'s. The most general method for finding the

probability function for some function of random variables

and

and

involves looking at every combination

involves looking at every combination

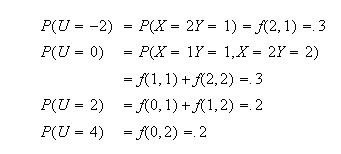

to see what value the function takes. For example, if we let

to see what value the function takes. For example, if we let

in our example, the possible values of

in our example, the possible values of

are seen by looking at the value of

are seen by looking at the value of

for each

for each

in the range of

in the range of

.

.

The probability function of

is thus

is thus

|

-2 |

0 |

2 |

4 |

|

.3 |

.3 |

.2 |

.2 |

For some functions it is possible to approach the problem more systematically.

One of the most common functions of this type is the total. Let

.

This gives:

.

This gives:

Then

,

for example. Continuing in this way, we get

,

for example. Continuing in this way, we get

|

1 |

2 |

3 |

4 |

|

.1 |

.4 |

.4 |

.1 |

(We are being a little sloppy with our notation by using

" " for

both

" for

both

and

and

.

No confusion arises here, but better notation would be to write

.

No confusion arises here, but better notation would be to write

for

for

.)

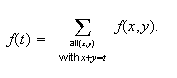

In fact, to find

.)

In fact, to find

we are simply adding the probabilities for all

we are simply adding the probabilities for all

combinations with

combinations with

.

This could be written as:

.

This could be written as:

However, if

,

then

,

then

.

To systematically pick out the right combinations of

.

To systematically pick out the right combinations of

,

all we really need to do is sum over values of

,

all we really need to do is sum over values of

and then substitute

and then substitute

for

for

.

Then,

.

Then,

So

would be

would be

(note

since

since

can't be 3.)

can't be 3.)

We can summarize the method of finding the probability function for a function

of two random variables

of two random variables

and

and

as follows:

as follows:

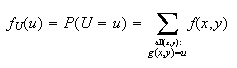

Let

be the probability function for

be the probability function for

.

Then the probability function for

.

Then the probability function for

is

is

This can also be extended to functions of three or more r.v.'s

This can also be extended to functions of three or more r.v.'s

:

:

(Note: Do not get confused between the functions

(Note: Do not get confused between the functions

and

and

in the above:

in the above:

is the joint probability function of the r.v.'s

is the joint probability function of the r.v.'s

whereas

whereas

defines the "new" random variable that is a function of

defines the "new" random variable that is a function of

and

and

,

and whose distribution we want to find.)

,

and whose distribution we want to find.)

This completes the introduction of the basic ideas for multivariate

distributions. As we look at harder problems that involve some algebra, refer

back to these simpler examples if you find the ideas no longer making sense to

you.

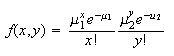

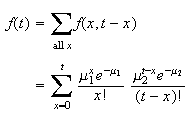

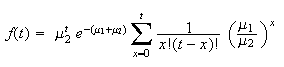

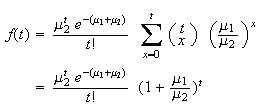

Example: Let

and

and

be independent random variables having Poisson distributions with averages

(means) of

be independent random variables having Poisson distributions with averages

(means) of

and

and

respectively. Let

respectively. Let

.

Find its probability function,

.

Find its probability function,

.

.

Solution: We first need to find

.

Since

.

Since

and

and

are independent we know

are independent we know

Using the Poisson probability function,

Using the Poisson probability function,

where

where

and

and

can equal 0, 1, 2,

can equal 0, 1, 2,

.

Now,

.

Now,

Then

Then

To evaluate this sum, factor out constant terms and try to regroup in some

form which can be evaluated by one of our summation techniques.

If we had a

on the top inside the

on the top inside the

,

the sum would be of the form

,

the sum would be of the form

.

This is the right hand side of the binomial theorem. Multiply top and bottom

by

.

This is the right hand side of the binomial theorem. Multiply top and bottom

by

to get:

to get:

Take a common denominator of

to get

to get

Note that we have just shown that the sum of 2 independent Poisson random

variables also has a Poisson

distribution.

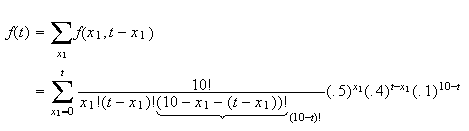

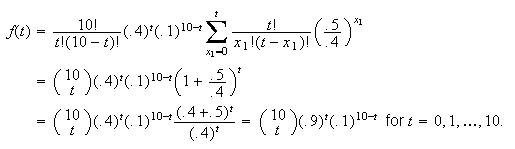

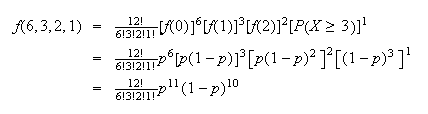

Example: Three sprinters,

and

and

,

compete against each other in 10 independent 100 m. races. The probabilities

of winning any single race are .5 for

,

compete against each other in 10 independent 100 m. races. The probabilities

of winning any single race are .5 for

,

.4 for

,

.4 for

,

and .1 for

,

and .1 for

.

Let

.

Let

and

and

be the number of races

be the number of races

and

and

win.

win.

-

Find the joint probability function,

-

Find the marginal probability function,

-

Find the conditional probability function,

-

Are

and

and

independent? Why?

independent? Why?

-

Let

.

Find its probability function,

.

Find its probability function,

.

.

Solution: Before starting, note that

since there are 10 races in all. We really only have two variables since

since there are 10 races in all. We really only have two variables since

.

However it is convenient to use

.

However it is convenient to use

to save writing and preserve symmetry.

to save writing and preserve symmetry.

-

The reasoning will be similar to the way we found the binomial distribution in

Chapter 6 except that there are now 3 types of outcome. There are

different outcomes (i.e. results for races 1 to 10) in which there are

different outcomes (i.e. results for races 1 to 10) in which there are

wins by

wins by

by

by

,

and

,

and

by

by

.

Each of these arrangements has a probability of (.5) multiplied

.

Each of these arrangements has a probability of (.5) multiplied

times, (.4)

times, (.4)

times, and (.1)

times, and (.1)

times in some order;

times in some order;

i.e.,

The range for

is triples

is triples

where each

where each

is an integer between 0 and 10, and where

is an integer between 0 and 10, and where

.

.

-

It would also be acceptable to drop

as a variable and write down the probability function for

as a variable and write down the probability function for

only; this is

only; this is

because of the fact that

because of the fact that

must equal

must equal

.

For this probability function

.

For this probability function

and

and

.

This simplifies finding

.

This simplifies finding

a little . We now have

a little . We now have

.

The limits of summation need care:

.

The limits of summation need care:

could be as small as

could be as small as

,

but since

,

but since

,

we also require

,

we also require

.

(E.g., if

.

(E.g., if

then

then

can win

can win

,

or 3 races.) Thus,

,

or 3 races.) Thus,

(Hint: In

the 2 terms in the denominator add to the term in the numerator, if we ignore

the ! sign.) Multiply top and bottom by

the 2 terms in the denominator add to the term in the numerator, if we ignore

the ! sign.) Multiply top and bottom by

This

gives

This

gives

Here

is defined for

is defined for

.

.

Note: While this derivation is included as an example of how

to find marginal distributions by summing a joint probability function, there

is a much simpler method for this problem. Note that each race is either won

by

(``success'') or it is not won by

(``success'') or it is not won by

(``failure''). Since the races are independent and

(``failure''). Since the races are independent and

is now just the number of ``success'' outcomes,

is now just the number of ``success'' outcomes,

must have a binomial distribution, with

must have a binomial distribution, with

and

and

.

.

Hence

for

for

,

as above.

,

as above.

-

Remember that

,

so that

,

so that

For any given value of

For any given value of

ranges through

ranges through

(So the range of

(So the range of

depends on the value

depends on the value

,

which makes sense: if

,

which makes sense: if

wins

wins

races then the most

races then the most

can win is

can win is

.)

.)

Note: As in (b), this result can be obtained more simply

by general reasoning. Once we are given that

wins

wins

races, the remaining

races, the remaining

races are all won by either

races are all won by either

or

or

.

For these races,

.

For these races,

wins

wins

of the time and

of the time and

of the time, because

of the time, because

and

and

;

i.e.,

;

i.e.,

wins 4 times as often as

wins 4 times as often as

.

More formally

.

More formally

from the binomial distribution.

from the binomial distribution.

-

and

and

are clearly not independent since the more races

are clearly not independent since the more races

wins, the fewer races there are for

wins, the fewer races there are for

to win. More

formally,

to win. More

formally, (In general, if the range for

(In general, if the range for

depends on the value of

depends on the value of

,

then

,

then

and

and

cannot be independent.)

cannot be independent.)

-

If

then

then

The upper limit on

is

is

because, for example, if

because, for example, if

then

then

could not have won more than 7 races. Then

could not have won more than 7 races. Then

What do we need to multiply by on the top and bottom? Can you spot it before

looking below?

Exercise: Explain to yourself how this answer can be

obtained from the binomial distribution, as we did in the notes following

parts (b) and (c).

The following problem is

similar to conditional probability problems that we solved in Chapter 4. Now

we are dealing with events defined in terms of random variables. Earlier

results give us things like

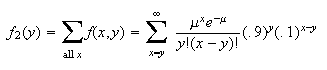

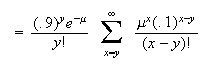

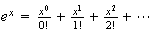

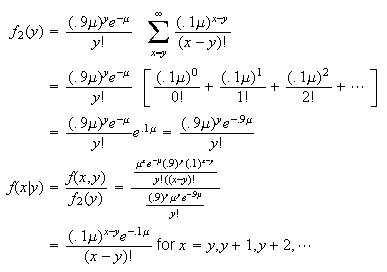

Example: In an auto parts company an average of

defective parts are produced per shift. The number,

defective parts are produced per shift. The number,

,

of defective parts produced has a Poisson distribution. An inspector checks

all parts prior to shipping them, but there is a 10% chance that a defective

part will slip by undetected. Let

,

of defective parts produced has a Poisson distribution. An inspector checks

all parts prior to shipping them, but there is a 10% chance that a defective

part will slip by undetected. Let

be the number of defective parts the inspector finds on a shift. Find

be the number of defective parts the inspector finds on a shift. Find

.

(The company wants to know how many defective parts are produced, but can only

know the number which were actually detected.)

.

(The company wants to know how many defective parts are produced, but can only

know the number which were actually detected.)

Solution: Think of

being event

being event

and

and

being event

being event

;

we want to find

;

we want to find

.

To do this we'll use

.

To do this we'll use

We know

We know

Also, for a given number

Also, for a given number

of defective items produced, the number,

of defective items produced, the number,

,

detected has a binomial distribution with

,

detected has a binomial distribution with

and

and

,

assuming each inspection takes place independently. Then

,

assuming each inspection takes place independently. Then

Therefore

Therefore

To get

To get

we'll need

we'll need

.

We have

.

We have

(

( since the number of defective items produced can't be less than the number

detected.)

since the number of defective items produced can't be less than the number

detected.)

We could fit this into the summation result

We could fit this into the summation result

by writing

by writing

as

as

.

Then

.

Then

Problems:

-

The joint probability function of

is:

is:

|

|

|

|

0 |

1 |

2 |

|

0 |

.09 |

.06 |

.15 |

|

1 |

.15 |

.05 |

.20 |

|

2 |

.06 |

.09 |

.15 |

-

Are

and

and

independent? Why?

independent? Why?

-

Tabulate the conditional probability function,

.

.

-

Tabulate the probability function of

.

.

-

In problem 6.14, given that

sales were made in a 1 hour period, find the probability function for

sales were made in a 1 hour period, find the probability function for

,

the number of calls made in that hour.

,

the number of calls made in that hour.

-

and

and

are independent, with

are independent, with

and

and

.

Let

.

Let

.

Find the probability function,

.

Find the probability function,

.

You may use the result

.

You may use the result

.

.

Multinomial Distribution

There is only this one multivariate model distribution introduced in this

course, though other multivariate distributions exist. The multinomial

distribution defined below is very important. It is a generalization of the

binomial model to the case where each trial has

possible outcomes.

possible outcomes.

Physical Setup: This distribution is the same as binomial

except there are

types of outcome rather than two. An experiment is repeated independently

types of outcome rather than two. An experiment is repeated independently

times with

times with

distinct types of outcome each time. Let the probabilities of these

distinct types of outcome each time. Let the probabilities of these

types be

types be

each time. Let

each time. Let

be the number of times the

be the number of times the

type occurs,

type occurs,

the number of times the

the number of times the

occurs,

occurs,

,

,

the number of times the

the number of times the

type occurs. Then

type occurs. Then

has a multinomial distribution.

has a multinomial distribution.

Notes:

-

-

,

,

If we wish we can drop one of the variables (say the last), and just note that

equals

equals

.

.

Illustrations:

-

In the example of Section 8.1 with sprinters A,B, and C running 10 races we

had a multinomial distribution with

and

and

.

.

-

Suppose student marks are given in letter grades as A, B, C, D, or F. In a

class of 80 students the number getting A, B, ..., F might have a multinomial

distribution with

and

and

.

.

Joint Probability Function: The joint probability function of

is given by extending the argument in the sprinters example from

is given by extending the argument in the sprinters example from

to general

to general

.

There are

.

There are

different outcomes of the

different outcomes of the

trials in which

trials in which

are of the

are of the

type,

type,

are of the

are of the

type, etc. Each of these arrangements has probability

type, etc. Each of these arrangements has probability

since

since

is multiplied

is multiplied

times in some order, etc.

times in some order, etc.

The restriction on the

The restriction on the

's

are

's

are

and

and

.

.

As a check that

we use the multinomial theorem to get

we use the multinomial theorem to get

We have already seen one example of the multinomial distribution in the

sprinter example.

Here is another simple example.

Example: Every person is one of four blood types: A, B, AB

and O. (This is important in determining, for example, who may give a blood

transfusion to a person.) In a large population let the fraction that has type

A, B, AB and O, respectively, be

.

Then, if

.

Then, if

persons are randomly selected from the population, the numbers

persons are randomly selected from the population, the numbers

of types A, B, AB, O have a multinomial distribution with

of types A, B, AB, O have a multinomial distribution with

(In Caucasian people the values of the

(In Caucasian people the values of the

's

are approximately

's

are approximately

)

)

Remark: We sometimes use the notation

to indicate that

to indicate that

have a multinomial

distribution.

have a multinomial

distribution.

Remark: For some types of problems its helpful to write

formulas in terms of

and

and

using the fact that

using the fact that

In this case we can write the joint p.f. as

In this case we can write the joint p.f. as

but we must remember then that

but we must remember then that

satisfy the condition

satisfy the condition

.

.

The multinomial distribution can also arise in combination with other models,

and students often have trouble recognizing it then.

Example: A potter is producing teapots one at a time. Assume

that they are produced independently of each other and with probability

the pot produced will be "satisfactory"; the rest are sold at a lower price.

The number,

the pot produced will be "satisfactory"; the rest are sold at a lower price.

The number,

,

of rejects before producing a satisfactory teapot is recorded. When 12

satisfactory teapots are produced, what is the probability the 12 values of

,

of rejects before producing a satisfactory teapot is recorded. When 12

satisfactory teapots are produced, what is the probability the 12 values of

will consist of six 0's, three 1's, two 2's and one value which is

will consist of six 0's, three 1's, two 2's and one value which is

?

?

Solution: Each time a "satisfactory" pot is produced the

value of

falls in one of the four categories

falls in one of the four categories

.

Under the assumptions given in this question,

.

Under the assumptions given in this question,

has a geometric distribution with

has a geometric distribution with

so we can find the probability for each of these categories. We have

so we can find the probability for each of these categories. We have

for

for

and we can obtain

and we can obtain

in various ways:

in various ways:

-

since we have a geometric series.

-

With some re-arranging, this also gives

With some re-arranging, this also gives

.

.

-

The only way to have

is to have the first 3 pots produced all being rejects.

is to have the first 3 pots produced all being rejects.

(3 consecutive rejects) =

(3 consecutive rejects) =

Reiterating that each time a pot is successfully produced, the value of

falls in one of 4 categories

falls in one of 4 categories

,

we see that the probability asked for is given by a multinomial distribution,

Mult

,

we see that the probability asked for is given by a multinomial distribution,

Mult :

:

Problems:

-

An insurance company classifies policy holders as class A,B,C, or D. The

probabilities of a randomly selected policy holder being in these categories

are .1, .4, .3 and .2, respectively. Give expressions for the probability that

25 randomly chosen policy holders will include

-

3A's, 11B's, 7C's, and 4D's.

-

3A's and 11B's.

-

3A's and 11B's, given that there are 4D's.

-

Chocolate chip cookies are made from batter containing an average of 0.6 chips

per c.c. Chips are distributed according to the conditions for a Poisson

process. Each cookie uses 12 c.c. of batter. Give expressions for the

probabilities that in a dozen cookies:

-

3 have fewer than 5 chips.

-

3 have fewer than 5 chips and 7 have more than 9.

-

3 have fewer than 5 chips, given that 7 have more than 9.

Markov Chains

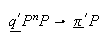

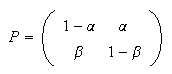

Consider a sequence of (discrete) random variables

each of which takes integer values

each of which takes integer values

(called states). We assume that for a certain matrix

(called states). We assume that for a certain matrix

(called the transition probability matrix), the conditional

probabilities are given by corresponding elements of the matrix; i.e.

(called the transition probability matrix), the conditional

probabilities are given by corresponding elements of the matrix; i.e.

and furthermore that the chain only uses the last state occupied in

determining its future; i.e. that

and furthermore that the chain only uses the last state occupied in

determining its future; i.e. that

for all

for all

and

and

.

Then the sequence of random variables

.

Then the sequence of random variables

is called a Markov Note_2

Chain. Markov Chain models are the most common simple models for

dependent variables, and are used to predict weather as well as movements of

security prices. They allow the future of the process to depend on the present

state of the process, but the past behaviour can influence the future only

through the present state.

is called a Markov Note_2

Chain. Markov Chain models are the most common simple models for

dependent variables, and are used to predict weather as well as movements of

security prices. They allow the future of the process to depend on the present

state of the process, but the past behaviour can influence the future only

through the present state.

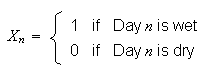

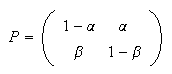

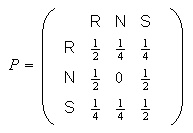

Example. Rain-No rain

Suppose that the probability that tomorrow is rainy given that today is not

raining is

(and it does not otherwise depend on whether it rained in the past) and the

probability that tomorrow is dry given that today is rainy is

(and it does not otherwise depend on whether it rained in the past) and the

probability that tomorrow is dry given that today is rainy is

If tomorrow's weather depends on the past only through whether today is wet or

dry, we can define random variables

If tomorrow's weather depends on the past only through whether today is wet or

dry, we can define random variables

(beginning at some arbitrary time origin, day

(beginning at some arbitrary time origin, day

). Then the random variables

). Then the random variables

form a Markov chain with

form a Markov chain with

possible states and having probability transition matrix

possible states and having probability transition matrix

Properties of the Transition Matrix

Note that

for all

for all

and

and

for all

for all

This last property holds because given that

This last property holds because given that

must occupy one of the states

must occupy one of the states

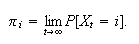

The distribution of

Suppose that the chain is started by randomly choosing a state for

with distribution

with distribution

.

Then the distribution of

.

Then the distribution of

is given by

is given by

and this is the

and this is the

element of the vector

element of the vector

where

where

is the column vector of values

is the column vector of values

.

To obtain the distribution at time

.

To obtain the distribution at time

premultiply the transition matrix

premultiply the transition matrix

by a vector representing the distribution at time

by a vector representing the distribution at time

Similarly the distribution of

Similarly the distribution of

is the vector

is the vector

where

where

is the product of the matrix

is the product of the matrix

with itself and the distribution of

with itself and the distribution of

is

is

Under very general conditions, it can be shown that these probabilities

converge because the matrix

Under very general conditions, it can be shown that these probabilities

converge because the matrix

converges pointwise to a limiting matrix as

converges pointwise to a limiting matrix as

In fact, in many such cases, the limit does not depend on the initial

distribution

In fact, in many such cases, the limit does not depend on the initial

distribution

because the limiting matrix has all of its rows identical and equal to some

vector of probabilities

because the limiting matrix has all of its rows identical and equal to some

vector of probabilities

Identifying this vector

Identifying this vector

when convergence holds is reasonably easy.

when convergence holds is reasonably easy.

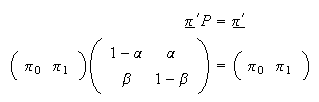

Definition

A limiting distribution of a Markov chain is a vector

( say) of long run probabilities of the individual states so

say) of long run probabilities of the individual states so

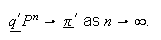

Now let us suppose that convergence to this distribution holds for a

particular initial distribution

Now let us suppose that convergence to this distribution holds for a

particular initial distribution

so we assume that

so we assume that

Then notice that

Then notice that

but also

but also

so

so

must have the property that

must have the property that

Any limiting distribution must have this property and this makes it easy in

many examples to identify the limiting behaviour of the chain.

Any limiting distribution must have this property and this makes it easy in

many examples to identify the limiting behaviour of the chain.

Definition

A stationary distribution of a Markov chain is the column vector

( say) of probabilities of the individual states such that

say) of probabilities of the individual states such that

.

.

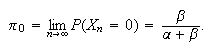

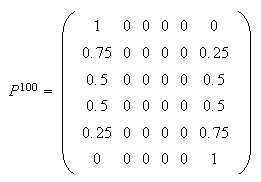

Example: (weather continued)

Let us return to the weather example in which the transition probabilities are

given by the matrix

What is the long-run proportion of rainy days? To determine this we need to

solve the equations

What is the long-run proportion of rainy days? To determine this we need to

solve the equations

subject to the conditions that the values

subject to the conditions that the values

are both probabilities (non-negative) and add to one. It is easy to see that

the solution

is

are both probabilities (non-negative) and add to one. It is easy to see that

the solution

is which is intuitively reasonable in that it says that the long-run probability

of the two states is proportional to the probability of a switch to that state

from the other. So the long-run probability of a dry day is the limit

which is intuitively reasonable in that it says that the long-run probability

of the two states is proportional to the probability of a switch to that state

from the other. So the long-run probability of a dry day is the limit

You might try verifying this by computing the powers of the matrix

You might try verifying this by computing the powers of the matrix

for

for

and show that

and show that

approaches the matrix

approaches the matrix

as

as

There are various mathematical conditions under which the limiting

distribution of a Markov chain unique and independent of the initial state of

the chain but roughly they assert that the chain is such that it forgets the

more and more distant past.

There are various mathematical conditions under which the limiting

distribution of a Markov chain unique and independent of the initial state of

the chain but roughly they assert that the chain is such that it forgets the

more and more distant past.

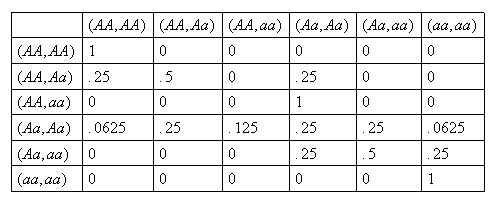

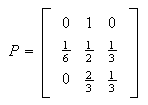

Example (Gene Model)

TA simple form of inheritance of traits occurs when a trait is governed by a

pair of genes

and

and

An

individual may have an

An

individual may have an

of an

of an

combination (in which case they are indistinguishable in appearance, or

"

combination (in which case they are indistinguishable in appearance, or

" dominates

dominates

.

Let us call an AA individual dominant,

.

Let us call an AA individual dominant,

recessive and

recessive and

hybrid. When two individuals mate, the offspring

inherits one gene of the pair from each parent, and we assume that these genes

are selected at random. Now let us suppose that two individuals of opposite

sex selected at random mate, and then two of their offspring mate, etc. Here

the state is determined by a pair of individuals, so the states of our process

can be considered to be objects like

hybrid. When two individuals mate, the offspring

inherits one gene of the pair from each parent, and we assume that these genes

are selected at random. Now let us suppose that two individuals of opposite

sex selected at random mate, and then two of their offspring mate, etc. Here

the state is determined by a pair of individuals, so the states of our process

can be considered to be objects like

indicating that one of the pair is

indicating that one of the pair is

and the other is

and the other is

(we do not distinguish the order of the pair, or male and female-assuming

these genes do not depend on the sex of the individual)

(we do not distinguish the order of the pair, or male and female-assuming

these genes do not depend on the sex of the individual)

For example, consider the calculation of

In this case each offspring has probability

In this case each offspring has probability

of being a dominant

of being a dominant

,

and probability of

,

and probability of

of being a hybrid

(

of being a hybrid

( ).

If two offspring are selected independently from this distribution the

possible pairs are

).

If two offspring are selected independently from this distribution the

possible pairs are

with probabilities

with probabilities

respectively. So the transitions have probabilities

below:

respectively. So the transitions have probabilities

below:

and transition probability

matrix

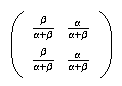

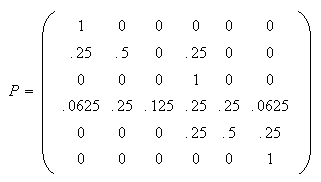

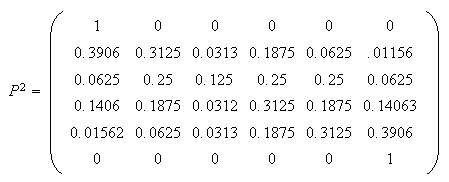

![$\allowbreak$]() What is the long-run behaviour in such a system? For example, the

two-generation transition probabilities are given by

What is the long-run behaviour in such a system? For example, the

two-generation transition probabilities are given by

which seems to indicate a drift to one or other of the extreme states 1 or 6.

To confirm the long-run behaviour calculate and :

which seems to indicate a drift to one or other of the extreme states 1 or 6.

To confirm the long-run behaviour calculate and :

which shows that eventually the chain is absorbed in either of state 1 or

state 6, with the probability of absorption depending on the initial state.

This chain, unlike the ones studied before, has more than one possible

stationary distributions, for example,

which shows that eventually the chain is absorbed in either of state 1 or

state 6, with the probability of absorption depending on the initial state.

This chain, unlike the ones studied before, has more than one possible

stationary distributions, for example,

and

and

and

in these circumstances the chain does not have the same limiting distribution

regardless of the initial state.

and

in these circumstances the chain does not have the same limiting distribution

regardless of the initial state.

Extension of Expectation to Multivariate Distributions

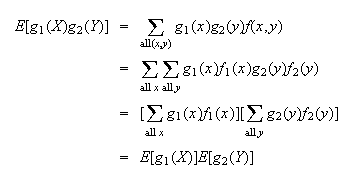

It is easy to extend the definition of expectation to multiple variables.

Generalizing

leads to the definition of expected value in the multivariate case

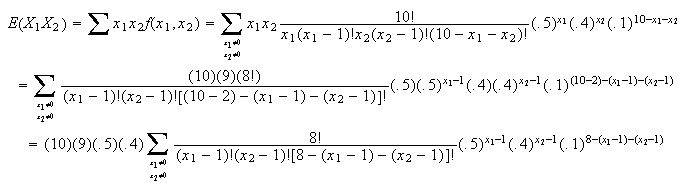

leads to the definition of expected value in the multivariate case

Definition

and

and

As before, these represent

the average value of

and

and

.

.

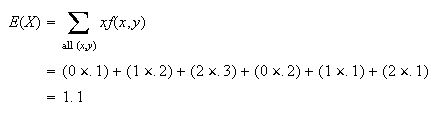

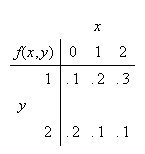

Example: Let the joint probability function,

,

be given by

,

be given by

|

|

|

|

0 |

1 |

2 |

|

1 |

.1 |

.2 |

.3 |

|

2 |

.2 |

.1 |

.1 |

Find

and

and

.

.

Solution:

To find

we have a choice of methods. First, taking

we have a choice of methods. First, taking

we

get

we

get Alternatively, since

Alternatively, since

only involves

only involves

,

we could find

,

we could find

and use

and use

Example: In the example of Section 8.1 with sprinters A, B,

and C we had (using only

and

and

in our formulas)

in our formulas)

where A wins

where A wins

times and B wins

times and B wins

times in 10 races. Find

times in 10 races. Find

.

.

Solution: This will be similar to the way

we derived the mean of the binomial distribution but, since this is a

multinomial distribution, we'll be using the multinomial theorem to sum.

Let

Let

and

and

in the sum and we obtain

in the sum and we obtain

Property of Multivariate

Expectation: It is easily proved (make sure you can do this) that

This can be extended beyond 2 functions

This can be extended beyond 2 functions

and

and

,

and beyond 2 variables

,

and beyond 2 variables

and

and

.

.

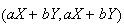

Relationships between Variables:

Independence is a "yes/no" way of defining a relationship between variables.

We all know that there can be different types of relationships between

variables which are dependent. For example, if

is your height in inches and

is your height in inches and

your height in centimetres the relationship is one-to-one and linear. More

generally, two random variables may be related (non-independent) in a

probabilistic sense. For example, a person's weight

your height in centimetres the relationship is one-to-one and linear. More

generally, two random variables may be related (non-independent) in a

probabilistic sense. For example, a person's weight

is not an exact linear function of their height

is not an exact linear function of their height

,

but

,

but

and

and

are nevertheless related. We'll look at two ways of measuring the strength of

the relationship between two random variables. The first is called covariance.

are nevertheless related. We'll look at two ways of measuring the strength of

the relationship between two random variables. The first is called covariance.

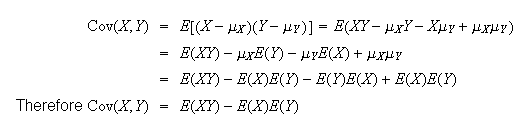

For calculation purposes

this definition is usually harder to use than the formula which follows, which

is proved noting that

Example:

In the example with joint probability function

find Cov

find Cov

.

.

Solution: We previously calculated

and

and

.

Similarly,

.

Similarly,

Exercise: Calculate the covariance of

and

and

for the sprinter example. We have already found that

for the sprinter example. We have already found that

= 18. The marginal distributions of

= 18. The marginal distributions of

and of

and of

are models for which we've already derived the mean. If your solution takes

more than a few lines you're missing an easier solution.

are models for which we've already derived the mean. If your solution takes

more than a few lines you're missing an easier solution.

Interpretation of Covariance:

-

Suppose large values of

tend to occur with large values of

tend to occur with large values of

and small values of

and small values of

with small values of

with small values of

.

Then

.

Then

and

and

will tend to be of the same sign, whether positive or negative. Thus

will tend to be of the same sign, whether positive or negative. Thus

will be positive. Hence Cov

will be positive. Hence Cov

.

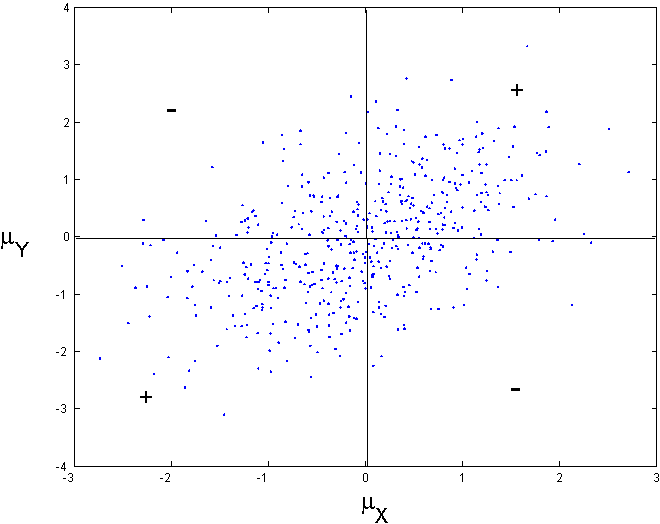

For example in Figure bivariatenormal we

see several hundred points plotted. Notice that the majority of the points

are in the two quadrants (lower left and upper right) labelled with "+" so

that for these

.

For example in Figure bivariatenormal we

see several hundred points plotted. Notice that the majority of the points

are in the two quadrants (lower left and upper right) labelled with "+" so

that for these

A minority of points are in the other two quadrants labelled "-" and for

these

A minority of points are in the other two quadrants labelled "-" and for

these

.

Moreover the points in the latter two quadrants appear closer to the mean

.

Moreover the points in the latter two quadrants appear closer to the mean

indicating that on average, over all points generated

indicating that on average, over all points generated

Presumably this implies that over the joint distribution of

Presumably this implies that over the joint distribution of

or

or

Random points

( with covariance 0.5, variances 1.

with covariance 0.5, variances 1.

|

For example of

person's

height and

person's

height and

person's

weight, then these two random variables will have positive covariance.

person's

weight, then these two random variables will have positive covariance.

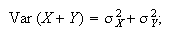

-

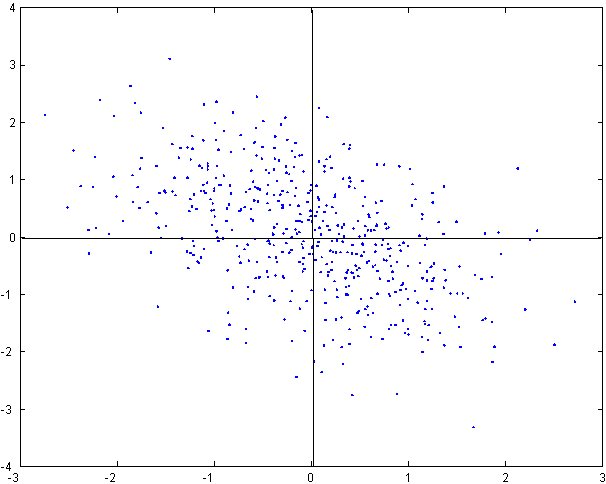

Suppose large values of

tend to occur with small values of

tend to occur with small values of

and small values of

and small values of

with large values of

with large values of

.

Then

.

Then

and

and

will tend to be of opposite signs. Thus

will tend to be of opposite signs. Thus

tends to be negative. Hence Cov

tends to be negative. Hence Cov

.

For example see Figure bivariatenormal2

.

For example see Figure bivariatenormal2

|

Covariance=-0.5,

variances=1

|

For example if

thickness

of attic insulation in a house and

thickness

of attic insulation in a house and

heating

cost for the house, then

heating

cost for the house, then

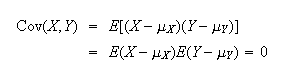

Proof: Recall

.

Let

.

Let

and

and

be independent.

be independent.

Then

.

.

The following theorem gives a direct proof the result above, and is useful in

many other situations.

Proof: Since

and

and

are independent,

are independent,

.

Thus

.

Thus

\framebox[0.10in]{}

\framebox[0.10in]{}

To prove result (3) above, we just note that if

and

and

are independent then

are independent then

Caution: This result is not reversible. If Cov

we can not conclude that

we can not conclude that

and

and

are independent. For example suppose that the random variable

are independent. For example suppose that the random variable

is uniformly distributed on the values

is uniformly distributed on the values

and define

and define

and

and

It is easy to see that

Cov

It is easy to see that

Cov but the two random variables

but the two random variables

are clearly related because the points

are clearly related because the points

are always on a circle.

are always on a circle.

Example: Let

have the joint probability function

have the joint probability function

;

i.e.

;

i.e.

only takes 3 values.

only takes 3 values.

|

0 |

1 |

2 |

|

.2 |

.6 |

.2 |

and

|

0 |

1 |

|

.4 |

.6 |

are marginal probability functions. Since

therefore,

therefore,

and

and

are not independent. However,

are not independent. However,

So

So

and

and

have covariance 0 but are not independent. If Cov

have covariance 0 but are not independent. If Cov

we say that

we say that

and

and

are uncorrelated, because of the definition of correlation

Note_3 given below.

are uncorrelated, because of the definition of correlation

Note_3 given below.

-

The actual numerical value of Cov

has no interpretation, so covariance is of limited use in measuring

relationships.

has no interpretation, so covariance is of limited use in measuring

relationships.

Exercise:

-

Look back at the example in which

was tabulated and Cov

was tabulated and Cov

.

Considering how covariance is interpreted, does it make sense that Cov

.

Considering how covariance is interpreted, does it make sense that Cov

would be negative?

would be negative?

-

Without looking at the actual covariance for the sprinter exercise, would you

expect Cov

to be positive or negative? (If A wins more of the 10 races, will B win more

races or fewer races?)

to be positive or negative? (If A wins more of the 10 races, will B win more

races or fewer races?)

We now consider a second, related way to measure the strength of relationship

between

and

and

.

.

The correlation coefficient measures the strength of the linear relationship

between

and

and

and is simply a rescaled version of the covariance, scaled to lie in the

interval

and is simply a rescaled version of the covariance, scaled to lie in the

interval

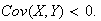

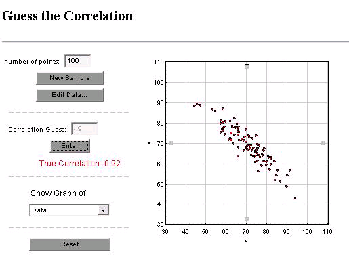

![$[-1,1].$](graphics/noteschap8__736.png) You can attempt to guess the correlation between two variables based on a

scatter diagram of values of these variables at the web

page

You can attempt to guess the correlation between two variables based on a

scatter diagram of values of these variables at the web

page

http://statweb.calpoly.edu/chance/applets/guesscorrelation/GuessCorrelation.html

For

example in Figure guesscorrelation I

guessed a correlation of -0.9 whereas the true correlation coefficient

generating these data was

|

Guessing the correlation

based on a scatter diagram of points

|

Properties of

:

:

-

Since

and

and

,

the standard deviations of

,

the standard deviations of

and

and

,

are both positive,

,

are both positive,

will have the same sign as Cov

will have the same sign as Cov

.

Hence the interpretation of the sign of

.

Hence the interpretation of the sign of

is the same as for Cov

is the same as for Cov

,

and

,

and

if

if

and

and

are independent. When

are independent. When

we say that

we say that

and

and

are uncorrelated.

are uncorrelated.

-

and as

and as

the relation between

the relation between

and

and

becomes one-to-one and linear.

becomes one-to-one and linear.

Proof: Define a new random variable

,

where

,

where

is some real number. We'll show that the fact that

Var

is some real number. We'll show that the fact that

Var leads to 2) above. We

have

leads to 2) above. We

have

Since

for any real number

for any real number

this quadratic equation must have at most one real root (value of

this quadratic equation must have at most one real root (value of

for which it is zero). Therefore

for which it is zero). Therefore

leading to the inequality

leading to the inequality

To see that

To see that

corresponds to a one-to-one linear relationship between

corresponds to a one-to-one linear relationship between

and

and

,

note that

,

note that

corresponds to a zero discriminant in the quadratic equation. This means that

there exists one real number

corresponds to a zero discriminant in the quadratic equation. This means that

there exists one real number

for which

for which

But for

Var

But for

Var to be zero,

to be zero,

must equal a constant

must equal a constant

.

Thus

.

Thus

and

and

satisfy a linear relationship.

satisfy a linear relationship.

Exercise: Calculate

for the sprinter example. Does your answer make sense? (You should already

have found Cov

for the sprinter example. Does your answer make sense? (You should already

have found Cov

in a previous exercise, so little additional work is

needed.)

in a previous exercise, so little additional work is

needed.)

Problems:

-

The joint probability function of

is:

is:

|

|

|

|

0 |

1 |

2 |

|

0 |

.06 |

.15 |

.09 |

|

|

|

|

|

|

1 |

.14 |

.35 |

.21 |

Calculate the correlation coefficient,

.

What does it indicate about the relationship between

.

What does it indicate about the relationship between

and

and

?

?

-

Suppose that

and

and

are random variables with joint probability function:

are random variables with joint probability function:

|

|

|

|

|

2 |

4 |

6 |

|

-1 |

1/8 |

1/4 |

|

|

|

|

|

|

|

1 |

1/4 |

1/8 |

|

-

For what value of

are

are

and

and

uncorrelated?

uncorrelated?

-

Show that there is no value of

for which

for which

and

and

are independent.

are independent.

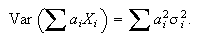

Mean and Variance of a Linear Combination of Random Variables

Many problems require us to consider linear combinations of random variables;

examples will be given below and in Chapter 9. Although writing down the

formulas is somewhat tedious, we give here some important results about their

means and variances.

Results for Means:

-

,

when

,

when

and

and

are constants. (This follows from the definition of expectation.) In

particular,

are constants. (This follows from the definition of expectation.) In

particular,

and

and

.

.

-

Let

be constants (real numbers) and

be constants (real numbers) and

.

Then

.

Then

.

In particular,

.

In particular,

.

.

-

Let

be random variables which have mean

be random variables which have mean

.

(You can imagine these being some sample results from an experiment such as

recording the number of occupants in cars travelling over a toll bridge.) The

sample mean is

.

(You can imagine these being some sample results from an experiment such as

recording the number of occupants in cars travelling over a toll bridge.) The

sample mean is

.

Then

.

Then

.

.

Proof: From (2),

.

Thus

.

Thus

Results for Covariance:

-

Cov

-

Cov

where

where

and

and

are constants.

are constants.

Proof:

This type of result can be generalized, but gets messy to write

out.

This type of result can be generalized, but gets messy to write

out.

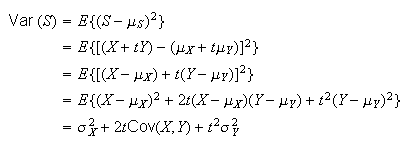

Results for Variance:

Proof:

Exercise: Try to prove this result by writing

as Cov

as Cov

and using properties of covariance.

and using properties of covariance.

-

Let

and

and

be independent. Since Cov

be independent. Since Cov

,

result 1. gives

,

result 1. gives

i.e., for independent variables, the variance of a sum

is the sum of the variances. Also note

i.e., for independent variables, the variance of a sum

is the sum of the variances. Also note

i.e., for independent variables, the variance of a difference is the

sum of the variances.

i.e., for independent variables, the variance of a difference is the

sum of the variances.

-

Let

be constants and Var

be constants and Var

.

Then

.

Then

This is a generalization of result 1. and can be proved using either of the

methods used for 1.

This is a generalization of result 1. and can be proved using either of the

methods used for 1.

-

Special cases of result 3. are:

-

If

are independent then Cov

are independent then Cov

,

so that

,

so that

-

If

are independent and all have the same variance

are independent and all have the same variance

,

then

,

then

Proof of 4 (b):

.

From 4(a), Var

.

From 4(a), Var

.

Using Var

.

Using Var

,

we get:

,

we get:

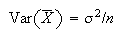

Remark: This result is a very important one in probability

and statistics. To recap, it says that if

are independent r.v.'s with the same mean

are independent r.v.'s with the same mean

and some variance

and some variance

,

then the sample mean

,

then the sample mean

has

has

This shows that the average

This shows that the average

of

of

random variables with the same distribution is less variable than any single

observation

random variables with the same distribution is less variable than any single

observation

,

and that the larger

,

and that the larger

is the less variability there is. This explains mathematically why, for

example, that if we want to estimate the unknown mean height

is the less variability there is. This explains mathematically why, for

example, that if we want to estimate the unknown mean height

in a population of people, we are better to take the average height for a

random sample of

in a population of people, we are better to take the average height for a

random sample of

persons than to just take the height of one randomly selected person. A sample

of

persons than to just take the height of one randomly selected person. A sample

of

persons would be better still. There are interesting applets at the url

http://users.ece.gatech.edu/users/gtz/java/samplemean/notes.html

and

http://www.ds.unifi.it/VL/VL_EN/applets/BinomialCoinExperiment.html which

allows one to sample and explore the rate at which the sample mean approaches

the expected value. In Chapter 9 we will see how to decide how large a sample

we should take for a certain degree of precision. Also note that as

persons would be better still. There are interesting applets at the url

http://users.ece.gatech.edu/users/gtz/java/samplemean/notes.html

and

http://www.ds.unifi.it/VL/VL_EN/applets/BinomialCoinExperiment.html which

allows one to sample and explore the rate at which the sample mean approaches

the expected value. In Chapter 9 we will see how to decide how large a sample

we should take for a certain degree of precision. Also note that as

,

which means that

,

which means that

becomes arbitrarily close to

becomes arbitrarily close to

.

This is sometimes called the "law of averages". There is a formal theorem

which supports the claim that for large sample sizes, sample means approach

the expected value, called the "law of large numbers".

.

This is sometimes called the "law of averages". There is a formal theorem

which supports the claim that for large sample sizes, sample means approach

the expected value, called the "law of large numbers".

Indicator Variables

The results for linear combinations of random variables provide a way of

breaking up more complicated problems, involving mean and variance, into

simpler pieces using indicator variables; an indicator variable is just a

binary variable (0 or 1) that indicates whether or not some event occurs.

We'll illustrate this important method with 3

examples.

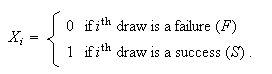

Example: Mean and Variance of a Binomial R.V.

Let

in a binomial process. Define new variables

in a binomial process. Define new variables

by:

by:

|

= |

0 if the

trial was a failure

trial was a failure |

|

= |

1 if the

trial was a success.

trial was a success. |

i.e.

indicates whether the outcome "success" occurred on the

indicates whether the outcome "success" occurred on the

trial. The trick we use is that the total number of successes,

trial. The trick we use is that the total number of successes,

,

is the sum of the

,

is the sum of the

's:

's:

We can find the mean and variance of

and then use our results for the mean and variance of a sum to get the mean

and variance of

and then use our results for the mean and variance of a sum to get the mean

and variance of

.

First,

.

First,

But

But

since the probability of success is

since the probability of success is

on each trial.

on each trial.

.

Since

.

Since

or 1,

or 1,

,

and therefore

,

and therefore

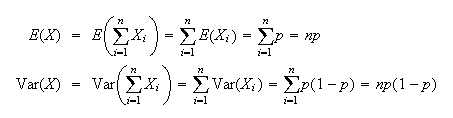

Thus

Thus

In the binomial distribution the trials are independent so the

's

are also independent. Thus

's

are also independent. Thus

These, of course, are the same as we derived previously for the mean and

variance of the binomial distribution. Note how simple the derivation here

is!

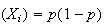

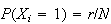

Remark: If

is a binary random variable with

is a binary random variable with

then

then

and

Var

and

Var ,

as shown above. (Note that

,

as shown above. (Note that

is actually a binomial r.v.) In some problems the

is actually a binomial r.v.) In some problems the

's

are not independent, and then we also need covariances.

's

are not independent, and then we also need covariances.

Example: Let

have a hypergeometric distribution. Find the mean and variance of

have a hypergeometric distribution. Find the mean and variance of

.

.

Solution: As above, let us think of the setting, which

involves drawing

items at random from a total of

items at random from a total of

,

of which

,

of which

are

"

are

" " and

" and

are

"

are

" items. Define

items. Define

Then

as for the binomial example, but now the

as for the binomial example, but now the

's

are dependent. (For example, what we get on the first draw affects the

probabilities of

's

are dependent. (For example, what we get on the first draw affects the

probabilities of

and

and

for the second draw, and so on.) Therefore we need to find

Cov

for the second draw, and so on.) Therefore we need to find

Cov for

for

as well as

as well as

and

Var

and

Var in order to use our formula for the variance of a sum.

in order to use our formula for the variance of a sum.

We see first that

for each of

for each of

.

(If the draws are random then the probability an

.

(If the draws are random then the probability an

occurs in draw

occurs in draw

is just equal to the probability position

is just equal to the probability position

is an

is an

when we arrange

when we arrange

's

and

's

and

's

in a row.) This immediately gives

's

in a row.) This immediately gives

since

since

The covariance of

The covariance of

and

and

is equal to

is equal to

,

so we need

,

so we need

The probability of an

The probability of an

on both draws

on both draws

and

and

is just

is just

Thus,

Thus,

(Does it make sense that Cov

(Does it make sense that Cov

is negative? If you draw a success in draw

is negative? If you draw a success in draw

,

are you more or less likely to have a success on draw

,

are you more or less likely to have a success on draw

?)

Now we find

?)

Now we find

and

Var

and

Var .

First,

.

First,

Before finding Var

Before finding Var

,

how many combinations

,

how many combinations

are there for which

are there for which

?

Each

?

Each

and

and

takes values from

takes values from

so there are

so there are

different combinations of

different combinations of

values. Each of these can only be written in 1 way to make

values. Each of these can only be written in 1 way to make

.

.

There are

There are

combinations with

combinations with

(e.g. if

(e.g. if

and

and

,

the combinations with

,

the combinations with

are (1,2) (1,3) and (2,3). So there are

are (1,2) (1,3) and (2,3). So there are

different combinations.)

different combinations.)

Now we can find

In the last two examples, we know

,

and could have found

,

and could have found

and

Var

and

Var without using indicator variables. In the next example

without using indicator variables. In the next example

is not known and is hard to find, but we can still use indicator variables for

obtaining

is not known and is hard to find, but we can still use indicator variables for

obtaining

and

and

.

The following example is a famous problem in probability.

.

The following example is a famous problem in probability.

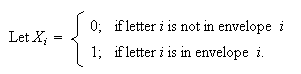

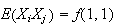

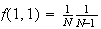

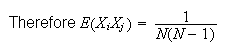

Example: We have

letters to

letters to

different people, and

different people, and

envelopes addressed to those

envelopes addressed to those

people. One letter is put in each envelope at random. Find the mean and

variance of the number of letters placed in the right envelope.

people. One letter is put in each envelope at random. Find the mean and

variance of the number of letters placed in the right envelope.

Solution:

Then

Then

is the number of correctly placed letters. Once again, the

is the number of correctly placed letters. Once again, the

's

are dependent (Why?).

's

are dependent (Why?).

First

(since there is 1 chance in

(since there is 1 chance in

that letter

that letter

will be put in envelope

will be put in envelope

)

and then,

)

and then,

Exercise: Before calculating cov

,

what sign do you expect it to have? (If letter

,

what sign do you expect it to have? (If letter

is correctly placed does that make it more or less likely that letter

is correctly placed does that make it more or less likely that letter

will be placed correctly?)

will be placed correctly?)

Next,

(As in the last example, this is the only non-zero term in the sum.) Now,

(As in the last example, this is the only non-zero term in the sum.) Now,

since once letter

since once letter

is correctly placed there is 1 chance in

is correctly placed there is 1 chance in

of letter

of letter

going in envelope

going in envelope

.

.

For the

covariance,

For the

covariance, (Common sense often helps in this course, but we have found no way of being

able to say this result is obvious. On average 1 letter will be correctly

placed and the variance will be 1, regardless of how many letters there are.)

(Common sense often helps in this course, but we have found no way of being

able to say this result is obvious. On average 1 letter will be correctly

placed and the variance will be 1, regardless of how many letters there are.)

Problems:

-

The joint probability function of

is given by:

is given by:

Calculate

Calculate

,

Var

,

Var

,

Cov

,

Cov

and Var

and Var

.

You may use the fact that

.

You may use the fact that

and Var

and Var

= .21 without verifying these figures.

= .21 without verifying these figures.

-

In a row of 25 switches, each is considered to be "on" or "off". The

probability of being on is .6 for each switch, independently of other switch.

Find the mean and variance of the number of unlike pairs among the 24 pairs of

adjacent switches.

-

Suppose Var

,

Var

,

Var

,

,

;

and let

;

and let

.

Find the standard deviation of

.

Find the standard deviation of

.

.

-

Let

be uncorrelated random variables with mean 0 and variance

be uncorrelated random variables with mean 0 and variance

.

Let

.

Let

.

Find Cov

.

Find Cov

for

for

and Var

and Var

.

.

-

A plastic fabricating company produces items in strips of 24, with the items

connected by a thin piece of plastic:

Item 1

--Item 2

-- ...

--Item 24

A cutting machine then

cuts the connecting pieces to separate the items, with the 23 cuts made

independently. There is a 10% chance the machine will fail to cut a connecting

piece. Find the mean and standard deviation of the number of the 24 items

which are completely separate after the cuts have been made. (Hint: Let

if item

if item

is not completely separate, and

is not completely separate, and

if item

if item

is completely separate.)

is completely separate.)

Multivariate Moment Generating Functions

Suppose we have two possibly dependent random variables

and we wish to characterize their joint distribution using a moment generating

function. Just as the probability function and the cumulative distribution

function are, in tis case, functions of two arguments, so is the moment

generating function.

and we wish to characterize their joint distribution using a moment generating

function. Just as the probability function and the cumulative distribution

function are, in tis case, functions of two arguments, so is the moment

generating function.

Definition

The joint moment generating function of

is

is

Recall that if

happen to be independent,

happen to be independent,

and

and

are any two functions,

are any two functions,

and so with

and so with

and

and